The almost two dozen above-the-line tax deductions get some tax return company this filing season. The One Big Beautiful Bill Act added four below-the-line deductions. And in all cases, the tax breaks are available to eligible taxpayers regardless of whether they itemize or claim the standard deduction.

We’ve mostly done away with paper nowadays, but reference to a line on the Internal Revenue Service’s Form 1040 tax return still is important at tax-filing time.

The line is 11a, the last one on page 1 of the individual income tax return. That’s where your adjusted gross income, or AGI, is entered.

There are two kinds of tax deductions related to the AGI entry.

Above-the-line deductions are those that come into play before the line 11a calculation. Most of these tax breaks, which have been around for ages, can reduce your AGI. And a smaller AGI could help you qualify for other tax breaks.

The below-the-line deductions, as the name indicates, come into effect after you determine your AGI. These amounts are subtracted from your AGI to arrive at your taxable income amount.

The One Big Beautiful Bill Act (OBBBA) added four temporary below-the-line deductions that can help qualifying individuals reduce how much they owe the U.S. Treasury.

Finally, both the above- and below-the-line deductions are available to qualifying filers regardless whether they itemize or take the standard tax deduction.

New below-the-line breaks: Since the OBBBA’s four below-the-line deductions are new this filing season, let’s start with them.

They are the exclusion of some tip income, no tax on certain overtime wages, a tax break for some specific auto loan interest payments, and the so-called Senior Bonus. You can find more on these (and some other OBBBA changes) in this earlier post on tax law changes that could affect your return filing.

If you qualify for any of these new below-the-line tax deductions, you’ll claim them on Form 1040 Schedule 1-A. This new form’s first section starts with your AGI, which you re-enter on line 11b, at the top of the 1040’s second page.

You’ll also have to enter other amounts, if applicable, such as foreign earned income and earnings from Puerto Rico and American Samoa you excluded. This will get you your modified adjusted gross income, or MAGI, amount. Your MAGI will determine how much of the new OBBBA deductions you can claim.

The next four sections, Parts II through V, walk you through the calculations — or the amounts are figured by your tax software or the tax pro you hired — to get to how much of each tax deduction you can claim related to your tips, overtime, vehicle loan interest, or for just reaching age 65.

These amounts then are transferred to your Form 1040 or Form 1040-SR if you’re an older taxpayer. Specifically, the entry goes on line 13b, which is, you got it, below the AGI line.

Again, you might not qualify for the full amount of the OBBBA’s new below-the-line deductions, but it’s worth the time to check them out, just in case.

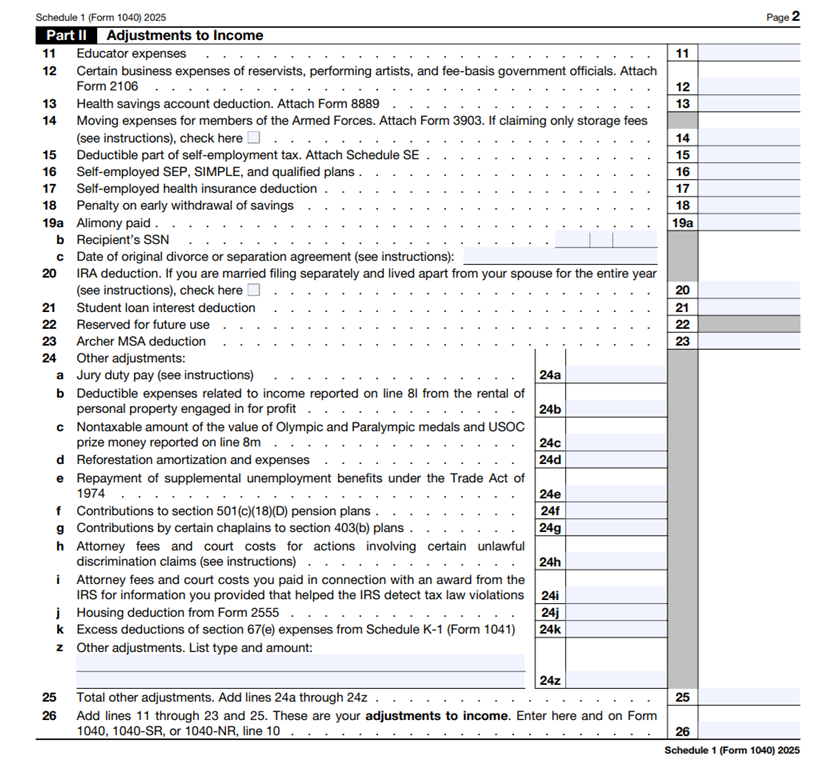

20+ familiar above-the-line deductions: Now to the old, and too often overlooked, above-the-line standbys. These tax breaks officially are known as Adjustments to Income. They are listed in Part II of Form 1040 Schedule 1, which is on the reverse, page 2 side of the schedule if you (like me) are looking at a paper form.

The above-the-line deductions used to be easy to find. Before the Tax Cuts and Jobs Act (TCJA) of 2017, they were listed right on Form 1040. But in 2018, the IRS created six new schedules for the main tax return, with Schedule 1 that year becoming the home of the above-the-line deductions.

Now, as noted, they are on a separate form, with this year’s version shown below.

Yes, I know some of these tax deductions are limited to very specific taxpayer situations. And yes, I know tax software walks you through your options. So does your tax pro.

But, being old school, I still like to look at the tax forms each year. And being a tax blogger, I want to make sure that readers don’t miss out on any tax breaks that could help them lessen what they owe Uncle Sam.

So, to that end, here’s a quick look at this year’s above-the-line deductions.

Educator expenses (line 11): Eligible educators can deduct some qualified unreimbursed classroom expenses paid out-of-pocket. The amount is adjusted annually for inflation. It’s $300 for the 2025 tax year. For teachers who like to plan ahead, it goes to $350 for 2026 expenditures.

So if you’re an eligible educator — the IRS says this includes kindergarten through grade 12 teachers, instructors, counselors, principals, or aides who worked in a school for at least 900 hours during a school year — don’t miss out on this deduction. One other note: home school parents don’t qualify for this deduction.

Certain business expenses (line 12): Don’t get too excited thinking this might help reduce your business tax bill. Schedule 1 notes that these write-offs are limited to folks in special job categories, specifically military reservists, performing artists and fee-basis government officials.

Also, reserve military personnel can only use this for costs incurred when they travel more than 100 miles from home to perform services as a National Guard or other armed forces reserve member. If you drove to these duties in 2025, those miles can be counted at 70 cents per mile. You also can add in parking, fees, and tolls. All taxpayers who take this deduction also will need to fill out Form 2106.

Health savings account deduction (line 13): Here you can write off your contributions to one of these medical coverage plans, commonly referred to as HSAs. You can check out the amount limits for 2025 filing and 2026 planning purposes. However, you’ll need more paperwork here, too. You must also file Form 8889.

Moving expenses for members of the Armed Forces (line 14): Folks who’ve claimed this tax break in the past probably noticed the added reference on this line’s description. It previously was shown only as moving expenses. But the TCJA changed that, too.

Now relocation costs are limited to military personnel who are on active duty and who move pursuant to a military order related to a permanent change of station. These relocating U.S. Armed forces members also will have to fill out Form 3903 to detail their eligible costs, the total of which go here.

Self-employment tax (line 15): If you worked for yourself, either as a full-time boss or via gigs to bring in some money to supplement your wage earnings, you likely had to pay self-employment tax. Half of that amount can be subtracted here. You’ll have to include your Schedule SE, too.

Self-employed SEP, SIMPLE, and qualified plans (line 16): Staying in the be-your-own-boss vein, if you were able to contribute to a qualified self-employment retirement plan, such as a SEP IRA or solo 401(k), note that amount here.

Self-employed health insurance deduction (line 17): One more break for the independent worker. If you paid for your own medical policy, those premiums are fully deductible here. The insurance also can cover your child who was younger than 27 at the end of 2025, even if the young person wasn’t your dependent. If you don’t use a tax pro or tax software (stop laughing; these tax unicorns are still out there), there’s a worksheet for the self-employed insurance deduction in the Form 1040 Schedule 1 instructions (page 94).

Penalty on early withdrawal of savings (line 18): If you had to cash in a CD or other savings plan and paid a price for getting your money from your bank, you can write off that fee here. You should have received a Form 1099-INT or Form 1099-OID detailing the early-withdrawal penalty amount.

Alimony paid (line 19): The 2017 tax reform law also changed the tax treatment of alimony for ex-spouses who pay and receive this money. But its changes don’t affect divorces that were granted before the tax law took effect. Those distinctions affect the entries on this three-part line.

Under the TCJA, the deduction for alimony payments — the amount entered on line 19a — will remain in effect for folks with divorce agreements finalized by a court and/or a formal divorce decree issued before the end of 2018. That’s why the date you enter on line 19c is so important.

As for the former spouse getting alimony, if your marital status change was on or after the TCJA’s Jan. 1, 2019, effective date for this provision, then you don’t owe tax on the spousal payments you get. If, however, it was before the law changed, you still owe Uncle Sam. That’s why line 19b wants your Social Security number, so the IRS can double check that you report it as income.

IRA deduction (line 20): If you have a traditional IRA, you might be able to deduct some or all of your contribution. This Schedule 1 deduction depends on many variables, such as income and workplace retirement plans, both for you and, if you’re married and file jointly, your spouse.

Student loan interest deduction (line 21): Student loans still bedevil many taxpayers. Changes to treatment of those loans as occupants of the Oval Office came and went have complicated matters. But the student loan interest has remained unchanged. Those paying down educational debt can write off up to $2,500 in interest on higher education loans here. You should get a Form 1098-E, Student Loan Interest Statement, from the school with the amount you paid. Also note that AGI limits affect how much you can enter on this line.

Reserved for future use (line 22): For all the abuse the IRS gets, it’s no fool when it comes to tax law changes. It’s painfully aware that Congress likes to fiddle with our filings, making more work for us taxpayers and IRS staff. That’s one reason this line is reserved. When Congress does eventually come up with another adjustment to income, it will be dropped in here.

Archer MSA deduction (line 23): An Archer MSA, short for medical savings account, was available only to certain self-employed people and small businesses. I say was because the Archer MSA program expired on Dec. 31, 2007. No new accounts were allowed after that date, but Archer MSAs established before then can continue to be used and receive contributions. The contributions can be claimed here, along with the filing of Form 8853.

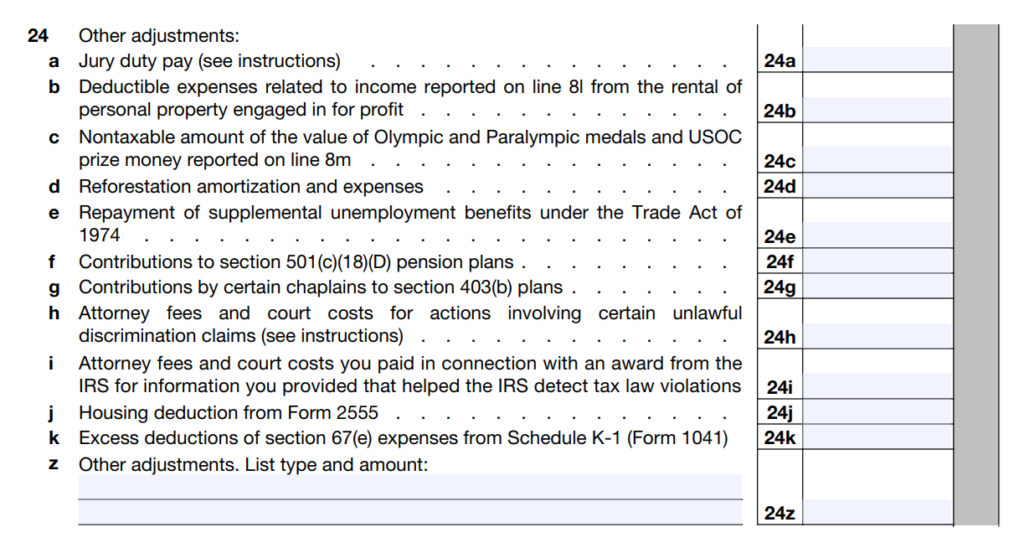

But wait, there’s more! Line 24, shown in the screenshot below, offers a dozen more changes to reduce your income as, what else, additional adjustments to income.

In case you’re reading this on a small device, the 12 additional income adjustments as alphabetic sublines of line 24 are:

- Jury duty pay if you gave the pay to your employer because your employer paid your salary while you served on the jury.

- Deductible expenses related to income reported on line 8l (that’s in Part 1 of Schedule 1’s Additional Income section) from the rental of personal property engaged in for profit.

- Nontaxable amount of the value of Olympic and Paralympic medals and USOC prize money reported on line 8m (again, in Part 1’s Additional Income section).

- Reforestation amortization and expenses (see instructions for Form 4562).

- Repayment of supplemental unemployment benefits under the Trade Act of 1974 (see IRS Publication 525).

- Contributions to section 501(c)(18)(D) pension plans (see IRS Publication 525).

- Contributions by certain chaplains to section 403(b) plans (see IRS Publication 517).

- Attorney fees and court costs for actions involving certain unlawful discrimination claims, but only to the extent of gross income from such actions (see IRS Publication 525).

- Attorney fees and court costs paid in connection with an award from the IRS for information you provided that helped the IRS detect tax law violations, up to the amount of the award includible in your gross income.

- Housing deduction from IRS Form 2555.

- Excess deductions of section 67(e) expenses from Schedule K-1 (Form 1041).

Finally, skipping from 24k to the end of the alphabet, (leaving room for possible future items on the schedule), we get the final possible above-the-line write-off, line 24z. It’s the always popular catchall entry, where you report any adjustments not entered elsewhere.

Here, the current IRS instructions say, “Leave line 24z blank.” No problem!

Once you add up all the adjustments, that total is transferred to line 10 of your 1040. (That line is shown in the first 1040 snippet shown back at the start of this post.) By subtracting these adjustments amount from your total income, you get your AGI.

More work, but tax savings: As with many tax breaks, claiming above-the-line deductions requires a bit more work. And, as noted, some of the tax breaks are very specific. But, again, tax software or your tax preparer can help.

And what’s a bit more work when it means you can shave a few more dollars off your final tax bill? Owing Uncle Sam as little as possible is, after all, the ultimate goal of all taxpayers.

{kind=link}