Mom often is the best doctor. But sometimes, we must turn to professional physicians and treatments. FSA money can help in these cases, as long as you didn’t lose the funds because you didn’t use them in time.

Yes, the holiday rush is still underway. Folks are returning or exchanging presents, redeeming gift certificates, and taking advantage of post-Christmas bargains.

Taxes are part of the shopping frenzy, too, if you have a flexible spending account.

These workplace medical spending accounts, usually referred to by their FSA acronym, are a great tax-advantaged way to pay for some medical costs. Employees contribute pre-tax dollars to the accounts. The funds then are used, tax-free, to pay for out-of-pocket health care expenses that are on the Internal Revenue Service’s qualified expenditure list.

But an FSA can literally be worthless if you don’t use the money in time. When that happens, the employee-contributed amount goes to the company offering the plan.

For many FSAs, that use-or-lose deadline is the last day of the year.

I know, I should have posted this earlier this month. But I was caught up in the pre-Christmas chaos. And admit it, so were you. The good thing is that it’s easy to spend down your FSA even with the Dec. 31 deadline looming. Here are some suggestions.

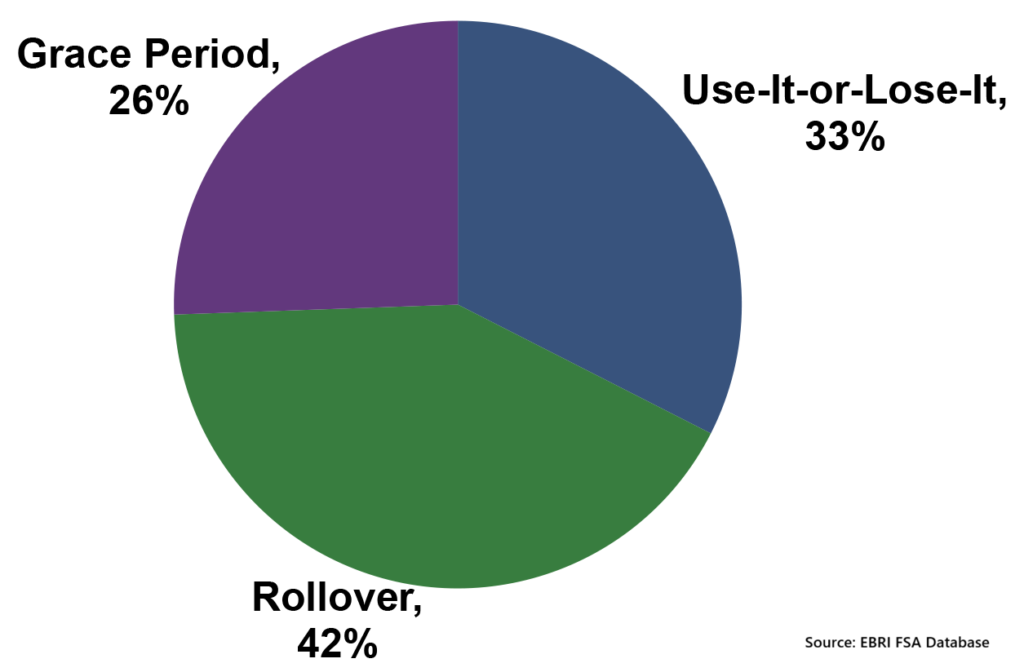

Other FSA usage deadlines: The end-of-year FSA deadline applies to a third of the workplace place accounts, according to the Employee Benefit Research Institute, or EBRI.

EBRI’s latest data show that the average FSA contribution in 2023 grew to $1,413. Most of the account owners — 88 percent — took a distribution.

Still, EBRI found that roughly half of FSA accountholders forfeited funds to their employer in 2023. The average amount they gave back was $436. Of the around 10 million Americans who abandon FSA funds, that unused money comes to more than $4 billion each year.

Some FSA holders, however, do get a bit of deadline relief.

Around a quarter of companies give their employee a bit more time to spend FSA funds. This grace period of 2½ months, or until March 15, means there’s no frantic grabbing of over-the-counter medications off store shelves on Dec. 31.

Then there’s the FSA rollover option, which the IRS made official back in 2013. Here, employers let their employees move a specific dollar amount from FSA at the end of the year into the next year. The maximum rollover amount is adjusted annually for inflation. For 2025, it’s $660. In 2026, it goes to $680.

But there’s a major caveat for both these extended FSA deadlines. They are optional.

The IRS says companies can offer either to their workers, but they don’t have to. And if a business decides to offer its FSA holding workings some flexibility on using the funds, it must choose one or the other. It can’t offer both a grace period and a rollover amount. So, if you’re unsure about whether you have a bit more time to spend all this year’s FSA money, talk to your benefits, payroll, or HR manager about your workplace’s rules.

Doctor, dentist, and other visits that qualify: Regardless of when you must use so you don’t lose your FSA funds, the money can only be used to pay for or reimburse expenditures on specific items.

If you already have an appointment with a medical professional, good, both for your health and your FSA considerations.

Any deductible or added costs for that tooth cleaning you put off until the last minute qualifies for FSA coverage. So do the prescription pain meds your dentist gives you if your procedure is more major, and ache inducing.

The same goes for treatments your primary care physician provides to help you recover from the flu you caught thanks to all those sneezing, coughing relatives you spent time with over the holidays.

Or maybe that nagging back pain you incurred by over-reaching during decoration installation just isn’t going away. Your chiropractor’s help in relieving the ache is a qualified medical expense.

Just make sure you have a legitimate health reason for any of your visits. The IRS says they must be for, the “diagnosis, cure, mitigation, treatment, or prevention of a specific medical condition.” Expenses for general wellness or maintenance are not FSA (or other medical deduction) eligible.

What about your eyes? Basic vision needs generally aren’t covered by workplace medical plans, but FSA funds can fill this gap. You can use the account money to buy prescription contacts, reading or regular glasses, or even sunglasses.

Note, however, the prescription requirement. You can’t just pick up a pair of cheap off-the-drugstore-display shades to look as cool as ZZ Top. Yeah, having to get medical treatments is not a fun way to wrap up a year, but it’s a good way to use up your FSA funds.

Prepare for emergencies: While most accidents don’t necessarily happen at home, despite the old saying, your abode can sometimes be treacherous. Note the reference earlier to the issue created by wrestling with that oversized inflatable Santa.

The chance for household accidents only increases during the holidays, when routines are disrupted and the house is full of people who are unfamiliar with the layout or simply just getting in each other’s way. You can be prepared, during the holiday season and year-round, by using your FSA funds to buy emergency supplies.

The easiest option here is a well-stocked first aid kit. It can help you take care of minor scrapes, like paper cuts from wrapping paper, to slight but painful burns when you picked up, sans potholder, the still-hot pie plate.

If you do need professional emergency treatment, your FSA money also can help cover hospital ER or urgent care visits, ambulance services to those facilities, and wheelchairs and slings if the accident was temporarily incapacitating.

Stock up on everyday illness items: If you want to build your own first aid kit, most of the supplies — bandages and Band-Aids, antiseptics, antibiotic creams, and the like — are available from at your local grocery or pharmacy.

A tax law change in 2011 to the Affordable Care Act (ACA), still known as Obamacare, made over-the-counter medications once again FSA eligible.

In addition to treating accident-caused injuries, the change means you can use FSA money for such items as pain relievers, cough and cold meds, thermometers, sleep aids, and digestive relief products.

Track miscellaneous medical costs: Don’t forget about all those Rx copays this year. Even if your insurance covers the prescribed medications, you usually face a deductible or copay. You can use your FSA money to pay these amounts.

The miles traveled to and from appointments, as well as the cost of tolls and parking, also can be reimbursed by your FSA. For the 2025 tax year, that’s a rate of 21 cents per mile.

Be sure to keep good records of these medical miles so you can verify any travel expense. Both the IRS and your FSA administrator accept travel costs only if they are in connection with medically necessary treatments and appointments.

Confirm allowed FSA expenses: The medically necessary caveat generally nixes such treatments as cosmetic surgery not related to a doctor’s diagnosis of a medical condition or dental procedures such as teeth whitening.

Many retailers help you identify FSA-eligible items by notating them on store shelves and even highlighting them on the register receipt. They also list the products on their websites.

You also can check FSA item eligibility at popular online marketplaces like FSA Store, Truemed, and Shop WealthCare that specialize in FSA-eligible items.

But the best way to find out what is covered by your FSA is to check with your plan’s administrator. That office usually has a list of what it will, and won’t, reimburse.

You can, of course, go straight to the source and review the IRS’ official documentation of allowable medical expenses, which generally are those that also can be claimed as itemized medical expenses on Schedule 1. The complete list is also known as IRS Publication 502.

Whenever your FSA spending deadline is, either by Dec. 31 or the first quarter of next year, make sure you meet it. You definitely don’t want to waste those dollars.

{kind=link}