Photo by Chris Ainsworth via Unsplash

Tax season 2026 officially began today. The Internal Revenue Service now is processing tax returns that millions submitted as soon as they could.

Some of us, however, are waiting to send in our 1040s. Most of us later filers are waiting for the official documentation we need to accurately complete our taxes.

And then there are the lucky few who don’t have to worry about the April 15 filing deadline.

Here’s a look at whether you might be among the select few legal nonfilers.

Basic filing requirements: For the most part, U.S. citizens and residents young, older and in-between, must file a tax return if they make money.

But the key is how much money they make. In addition, a person’s age and filing status come into play. The table below, taken from the Form 1040 instructions, shows how these three factors work together in determining whether you must file a 2025 tax year return by April 15 this year.

| If your filing status is: | AND at the end of 2025 you were: | THEN file a return if your gross income was at least: |

| Single | 64 or younger 65 or older | $15,750 $17,750 |

| Head of Household | 64 or younger 65 or older | $23,625 $25,625 |

| Married Filing Jointly | 64 or younger (both spouses) 65 or older (one spouse) 65 or older (both spouses) | $31,500 $33,100 $34,700 |

| Married Filing Separately | Any age | $5 |

| Qualifying surviving spouse | 64 or younger 65 or older | $31,500 $33,100 |

Now for a few notes on the table’s entries.

Age matters: Getting older also has a benefit when it comes to whether you have to file. As the table indicates, older individuals get to earn more money before the IRS requires a return.

The IRS also tweaks that age a bit to the advantage of older New Year’s Day babies. If you were born on Jan. 1, 1961, you are considered to be age 65 at the end of 2025.

That one-day shift lets you, as a de facto senior citizen, make a little more money before you have to file a return.

It doesn’t work the other way, though. You can’t be too young to file if you make enough money.

However, tax law does take into account other factors in figuring filing threshold amounts when someone is a tax dependent, which is the case for most young earners. More on this in a couple of paragraphs.

Type of earnings to count: As for the income level that triggers the need to file a 1040, that $5 amount for married filing separately spouses is not a typo.

If you’re married and you and your husband or wife file separate returns, then all it takes is earning five bucks for the IRS to demand that you, as a filer of your own separate 1040, file. This is one of the instances where the tax code encourages couples to stay wedded, bliss or not.

If you are one of the other filing status individuals and earn more than a five-spot a year, the IRS looks at your gross, or total income before deductions and adjustments. So the amounts in the table’s third column are all that you received during the tax year from all sources.

That includes the main payment method for most of us, money. That’s typically from a full-time, wage-paying job, but also covers earnings from side gigs that supplement to your salaried employment, or when you shifted completely to being your own boss.

Don’t forget about any capital gains, either from asset sales or distributions from mutual funds you kept in your portfolio.

And if you lived in a housing market where prices skyrocketed and you were able to sell before prices dropped, congratulations to you and possibly the IRS. Any home sale profit in excess of the residential exclusion amount ($250,000 for single owners, double that for jointly filing married home sellers) counts.

Older taxpayers also get another possible break in counting income that might require filing. Senior citizens don’t have to include any Social Security benefits unless —

- They are married filing a separate return and lived with their spouse at any time during 2025, or

- One-half of their Social Security benefits plus other gross income and any tax-exempt interest is more than $25,000 ($32,000 if married filing jointly).

In these cases, older individuals — or their tax software or tax preparers — must make some more calculations.

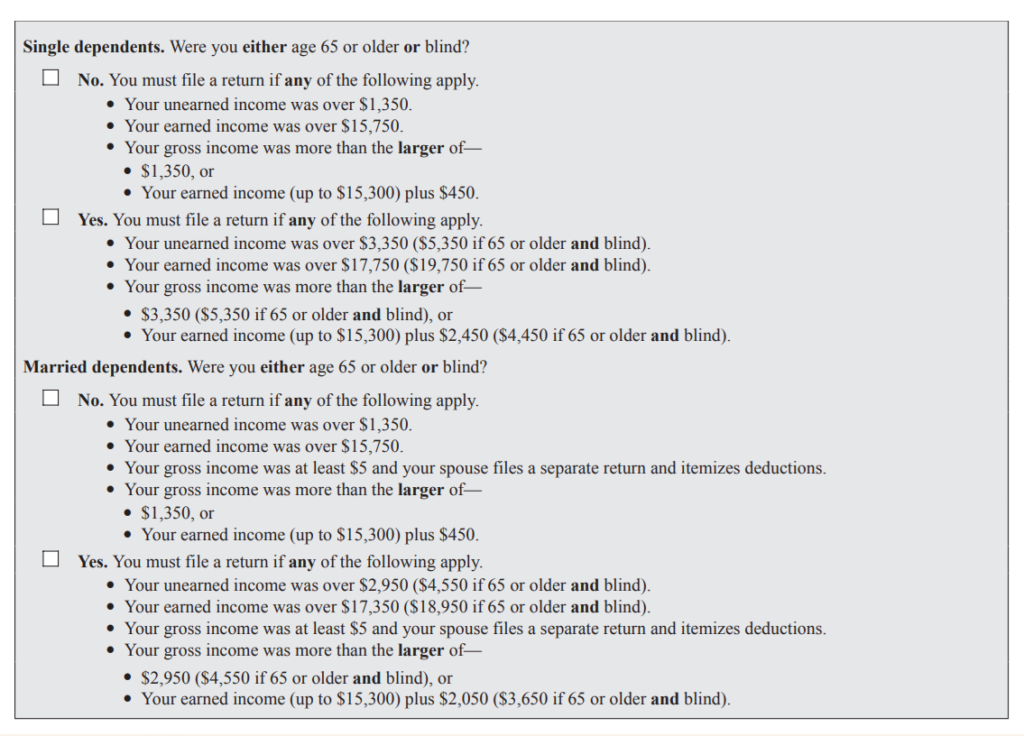

Dependent filer determinations: Now to those tax filing rules mentioned a bit earlier that apply to people, young and older, who are a dependent for tax purposes.

If your parent (or someone else) can claim you as a dependent, the IRS created the chart below, again published in the Form 1040 instructions, to help you figure out whether you must file a return.

Earned income cited in the above box includes salaries, wages, gratuities (more in a few paragraphs on the new One Big Beautiful Bill Act change that exempts a portion of some filers’ tips from taxation), professional fees, and taxable scholarship and fellowship grants.

The unearned income referred to includes taxable interest, ordinary dividends, and capital gain distributions. It also includes unemployment compensation, taxable Social Security benefits, pensions, annuities, and distributions of unearned income from a trust.

Gross income is the total of your unearned and earned income.

Other filing factors: But wait! There’s more. Other factors that, well, factor into the filing or not decision include the following.

- You made, after expenses, at least $400 from self-employment. This is an area where folks with side hustles need to pay close attention. While you might not technically have made enough to require filing a tax return, you still have to file in order to pay the self-employment (SE) tax on these independent earnings. The tax due here, calculated on Schedule SE, is the self-employed person’s version of the payroll taxes that go toward Social Security and Medicare, aka FICA, that are taken out of salaried workers’ checks. Again, it bears repeating. It’s possible you could owe SE taxes, but no income tax. However, you still must file to report those independent earnings.

- Your job includes gratuities, but you didn’t report all your tips to your employer. Of course, now some of that tip income is tax free for qualifying earners, so you’ll have to do some additional calculations. Since you didn’t tell your boss about these tips, the appropriate Federal Insurance Contributions Act (FICA) taxes weren’t withheld. So, you’ll owe income and the unpaid Social Security and Medicare tax due on any taxable portion of your unreported tips.

- You or your spouse or dependents got advance payments of the premium tax credit to help cover Affordable Care Act (ACA) medical coverage purchased through the healthcare Marketplace. Yes, these are the enhanced ACA, or Obamacare as it’s also known, subsidies that Congressional Republicans refused (so far) to extend this year. If, however, the tax break last year helped you pay for health care coverage, you must file to reconcile the health care credit amount you got upfront to buy your policy.

Household help filing requirements: You also face some filing tasks if you have household help and pay your employees enough to trigger employment taxes. I know, if you can hire help, you probably made enough to have to file a return anyway, and likely have a tax pro who helps make sure you file all the necessary forms on time.

But just in case, the IRS says that if in the 2025 tax year you paid $2,800 or more to individuals who helped in or around the house, you must file a Schedule H with your Form 1040. That threshold goes to $3,000 for the 2026 tax year.

Although the household help payment requirement is popularly called the nanny tax, it covers not just childcare assistance, but also maids, housekeepers, gardeners and others who provide services as your employee for the upkeep of your private residence.

Note, too, the employee characterization. This doesn’t apply to independent contractors who do household work for you, such as the housekeeper who comes in once a week or the monthly lawn service crew. But be careful here. The IRS looks closely at worker designations.

The good news, though, is that if you are filing a tax return only because you owe this tax, you can file Schedule H by itself, without having to hassle with a Form 1040.

More filing decision help: Finally (yes, finally!) there also are special tax filing rules for individuals whose spouse has died, executors, administrators, legal representatives, U.S. citizens and residents living outside the United States, residents of Puerto Rico, and individuals with income from U.S. territories.

You can find more about filing requirements in already cited Form 1040 instructions, as well as in IRS Publication 501 (although make sure it is for 2025 returns; at the time of this posting, IRS.gov still was linking to the prior tax year’s version), and of course, from your tax professional.

Don’t have a tax pro and don’t want to decipher all the filing rules’ tax-speak? No problem. You also can use the IRS’ online tool to determine whether you need to file a return this year.

Filing anyway: Finally, if you don’t have to file, you might want to anyway. This could be the case if, for example, you had more income tax withheld than you owe. The only way to get that money back from Uncle Sam is to send the IRS a Form 1040 with the details confirming your due tax refund.

That’s just one reason to file. There are more. But they are for another post, specifically tomorrow’s item.

UPDATE, Wednesday, Jan. 28, 2026: Tomorrow came and went. So did the next day, i.e., today. Both were dominated by some personal matters I had to handle. That’ll teach me to promise a specific date for posting!

So, let me just say now that I’ll see you back here soon for that installment of the ol’ blog’s tax season adventures.

UPDATE, Thursday, Jan. 29, 2026: The post on reasons to file even if the IRS doesn’t require it is live!

{kind=link}