Since the Supreme Court in 2018 let states allow betting on college sports, sportsbook activity, like this in a Las Vegas casino, has pick up substantially. (Photo by Kay Bell)

…

College and professional sports dominate screens right now. And sports wagering has increased annually since the Supreme Court of the United States in 2018 opened the door for states to allow sports betting on collegiate competitions.

The high court’s move also made it possible for the Internal Revenue Service to collect on winning bets placed at legal sportsbooks. For the most part, those operations report the amounts that went into their successful clients’ pockets.

But there’s still a whole lot of taxable betting cash slipping through Uncle Sam’s hands, according to a recent Treasury Inspector General for Tax Administration (TIGTA) report.

In fact, says TIGTA, “The IRS Could Collect Over a Billion Dollars in Taxes From Unreported Wagering Income.” And yes, as the capitalization (and linkage) indicates, that statement is the report’s official title.

Gross gambling revenue reaching an all-time high of $60.5 billion in 2022, notes the TIGTA report.

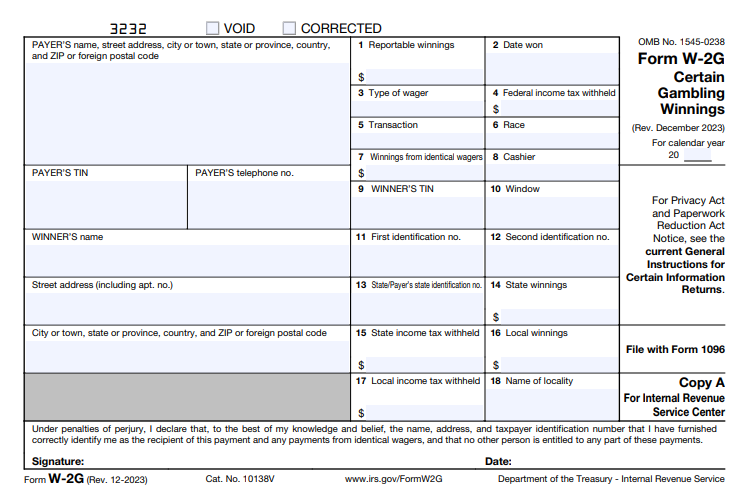

But, it adds, the IRS has not enforced income tax return filing requirements for those who received a Form W-2G, Certain Gambling Winnings (shown below). detailing how much they won. The W-2Gs are copied to the IRS.

See more tax forms and more about them at Tax Forms 2024.

…

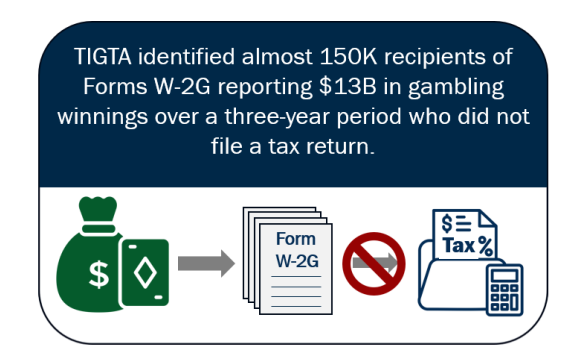

Taxpayers also gambling on IRS enforcement efforts: TIGTA reviewed all Forms W-2G issued to individual taxpayers during tax years 2018 through 2020 (as of March 2023).

During that period, 148,908 individuals who were issued W-2G forms totaling more than $15,000 per individual in gambling winnings did not file a tax return.

These nonfiling gamblers were associated with approximately $13.2 billion in total wagering winnings.

High earners not reporting winnings: Further TIGTA analysis determined that 139,045 of these nonfilers were included in the IRS’ nonfiler case creation process inventory.

And a significant portion of these nonfiling gamblers are high-income individuals. That means their taxable income, including wager wins, are in the higher income tax brackets.

IRS Commissioner Danny Werfel has emphasized the agency will be taking a closer look at the filings of these taxpayers. Part of the audit focus on wealthier taxpayers is to ensure tax compliance equity. It’s also a good way to collect more for the U.S. Treasury.

In response to TIGTA’s audit, the IRS analyzed 17,436 tax year 2018 high-income nonfilers with total positive income greater than or equal to $100,000 and calculated that it could potentially increase tax revenue by approximately $1.4 billion through addressing the 139,045 individual nonfilers with gambling winnings.

That uncollected $1.4 billion in potential tax revenue from high-earner winnings for 2018 alone earns this weekend’s By the Numbers [dis]honor.

No tax ID numbers: In addition, TIGTA found that hundreds of Forms W-2G do not include a Taxpayer Identification Number (TIN) required to trace the income to the recipient.

TIGTA also reported that the IRS has few processes in place to identify potential excise tax noncompliance by entities accepting wagers, particularly in emerging areas such as online sports wagering.

Finally, the report found that while the IRS has begun taking steps to address the uncollected gambling winnings issue, its enforcement remains inconsistent, especially in emergent gambling markets such as online sports betting.

TIGTA recommendations: As with most of its reports, TIGTA had some suggestions on how the IRS’ Small Business/Self-Employed Division could improve its compliance efforts when it comes to gambling income.

The tax watchdog’s five specific recommendations are that the IRS —

- Begin appropriate enforcement actions for nonfilers with gambling winnings from tax years 2018 through 2020;

- Review nonfilers with gambling winnings for that three-year time period who were not identified by the IRS’ nonfiler system;

- Analyze Forms W-2G with missing TINs to determine what forms of wagering and/or gambling institutions may be noncompliant;

- Expand the wager codes to specifically include sports betting; and

- Conduct an environment scan of the current and potential future conditions of the sports betting and online gambling industries.

IRS response: Amalia C. Colbert, IRS Commissioner for the Small Business/Self-Employed Division, detailed the agency’s response in her reply to the TIGTA audit. It is included as Appendix III in the report. Here’s a quick overview.

The IRS agreed with TIGTA recommendations 1, 2, and 5.

The tax agency will identify high-income nonfilers for tax years 2018 through 2020 with gambling winnings where no enforcement actions have been taken, including the top 100 nonfiler cases identified by TIGTA. If appropriate, the IRS will begin enforcement by issuing the first return delinquency notice.

As for the second recommendation, the IRS said it will review and profile the population of nonfilers with gambling winnings for 2018-2020 that were not identified by its Individual Master File Case Creation Nonfiler Identification Process (IMF CCNIP).

This research, says the IRS, will determine potential reasons why the nonfiler returns were not identified, and assess the current state of these returns to determine if the filing requirement has been satisfied. If the filing requirement has not been satisfied and enforcement is applicable, then manual enforcement of return delinquency will be considered.

The IRS also will, per TIGTA’s fifth recommendation, conduct an environment scan of the current and potential future conditions of the sports betting and online gambling industries, the industries’ risks, and impact on tax compliance. It also will update existing or create new charters to identify noncompliance.

It partially agreed to the fourth recommendation, and said it will explore the potential productivity and feasibility of expanding the wager codes to specifically include sports betting.

However, the IRS disagreed with analyzing Forms W-2G with missing TINs (recommendation #3) to determine what forms of wagering and/or gambling institutions may be noncompliant.

The reason for the rejection? IRS said TIGTA’s analysis identified a very insignificant percentage, .0010 percent of Forms W-2G with missing TINs. It also noted it has processes in place to identify and address compliance with information reporting, and considers TIGTA’s finding of an insignificant error rate to be a positive reflection of IRS efforts.

You also might find these items of interest:

- IRS Commissioner touts the tax agency’s generational digital transformation

- AI will be part of expansive IRS crackdown on wealthy, corporate tax evaders

- Are you ready for some football bets? Be sure to report your winnings on your tax return

Advertisements

🌟 Search Amazon Electronics 🌟

The text link above is an affiliate ad. If you click through and then buy a product, I receive a commission.

{kind=link}