Since the Social Security Administration (SSA) is a government agency, its Facebook page doesn’t have the relationship section.

But maybe it should.

The SSA definitely is involved in the lives of the more than 75 million people who get some sort of Social Security benefits. Millions of workers (and employers) also pay into the system through Federal Insurance Contributions Act (FICA) payroll taxes.

And when it comes to taxes, the SSA’s honest relationship assessment would have to be “It’s complicated.”

That status definitely applies at the federal level, both to the amounts individuals pay into the Social Security system and the taxes that Uncle Sam collects from some on their benefits.

It’s also complicated in the handful of states that tax the federal retirement payouts.

Here’s a look at these potentially taxable, and complicated, Social Security situations.

More benefits, more tax: Let’s start with when federal taxes are due on Social Security benefits, since the SSA just announced last week that those benefits will be increasing by 2.8 percent next year.

The good news is that not all your Social Security benefits are taxable. But depending on your overall income, Uncle Sam will want a cut.

Generally, if Social Security is all that you’re living on, then you don’t have to worry about filing a return. Those payments are tax-exempt.

If, however, your Social Security is supplemented by other income, either earned or unearned, you might — okay, probably will — owe taxes on some of the benefits. Basically, the greater your total amount of benefits and other income, the greater the taxable part of your benefits.

In these situations, up to 50 percent of Social Security benefits could be taxable. Recipients who have a larger nest egg to supplement the federal retirement payments could see up to 85 percent of their Social Security taxed.

Adding up what is taxed: More on those taxable percentages in a minute. First, let’s start with your benefits total.

The good news is that some, but not all of your Social Security benefits are subject to federal tax. The portion of your benefits that may be taxable varies since it depends on what the Internal Revenue Service calls your combined income.

This is your adjusted gross income (AGI), plus nontaxable interest and half of your annual Social Security benefits. You’ll find all the non-Social Security income to use in your calculation on your tax return.

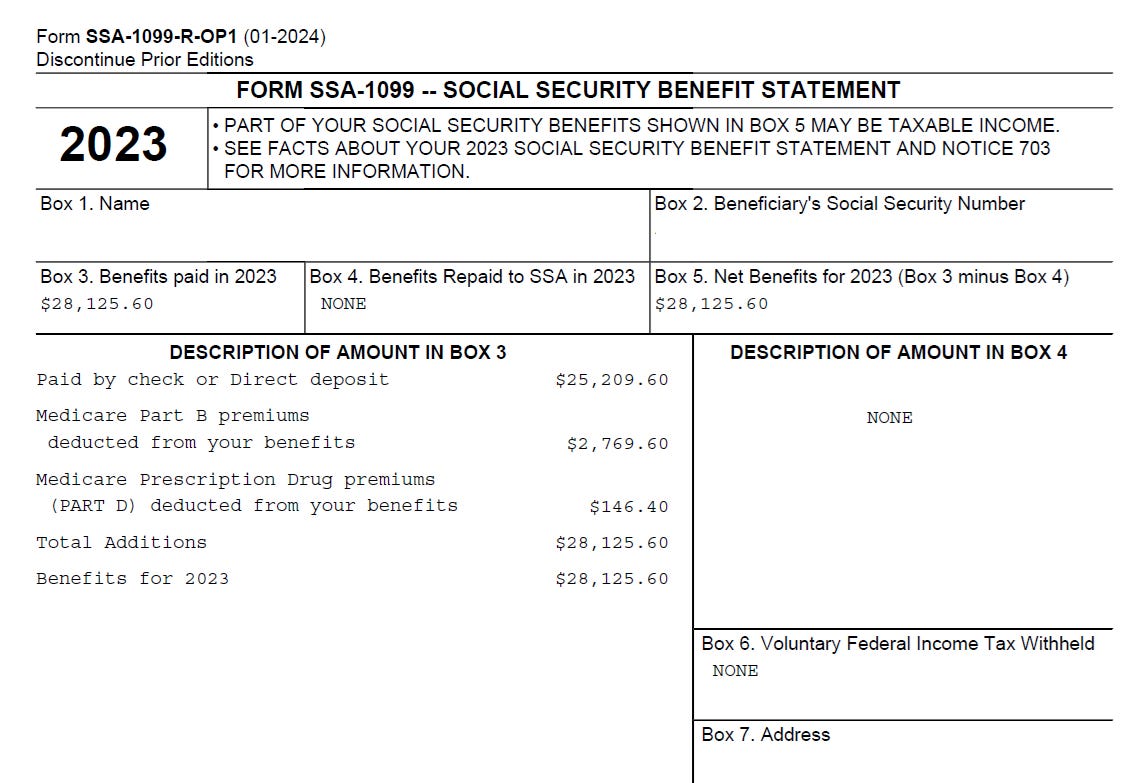

As for your federal retirement annual amount, the SSA will send you Form SSA-1099, Social Security Benefit Statement in January. If it doesn’t show up in your curbside U.S. Postal Service mailbox, which could happen since the Trump administration is looking to make as many government interactions as possible electronic, check your Social Security online account and download your SSA-1099 copy.

As the form excerpt example below shows, the SSA-1099 enters the amount of Social Security payments you received the previous year in box 5.

Then add one-half of that box 5 amount to, as noted earlier, your AGI and nontaxable interest. You’ll compare this combined income amount to the base amount for your filing status to determine if you owe tax, and if so, how much, on your Social Security benefits.

Base income, taxable percentages: The base amounts depend on your filing status.

If you file as an individual — this includes the single, head of household and qualifying widow(er) filing statuses — and your combined income is between $25,000 and $34,000, you must pay tax on up to 50 percent of your Social Security benefits.

Up to 85 percent of an individual’s benefits are taxable when combined income is more than $34,000.

Married couples who file a joint return may have to pay taxes on 50 percent of benefits if spouses have a combined income that is between $32,000 and $44,000.

Joint filers with income of more than $44,000 will see up to 85 percent of your Social Security benefits to be subject to income tax.

And if you’re married, but you and your spouse don’t file a combined 1040, the complicated description definitely comes into play in determining taxes on your Social Security benefits.

Married filing separately taxpayers who did not live with their spouses at any time during the tax year have the same base amount as individual filers. If, however, spouses lived together at any time during the tax year but just didn’t want to file together, the base amount is zilch. That’s right, zero dollars.

No indexing: The base income amounts are a major frustration for many — okay, most; okay all — of the taxpayers who end up owing tax on their federal retirement benefits, and not just because of the added calculations’ complications.

Retirees who end up owing tax on their benefits share a common criticism. The base amounts that lead to Social Security taxation aren’t adjusted for inflation. That means that even small Social Security cost-of-living bumps could push a filer into owing tax on the benefits.

Taxpayers who’ve saved for their golden years also complain that the process and static base amounts penalize them for being financially responsible for their retirement.

But, that’s an issue for Congress and another post.

Final calculations, possible withholding: You can figure your taxable Social Security amount using your tax software or the worksheet in the Form 1040 instruction book.

The IRS also has an online interactive tool to help you figure out if your federal retirement benefits are taxable and if so, just how much.

If you discover you owe tax on your Social Security, you have a couple of options.

You can pay the tax amount through quarterly estimated tax payments. Or you can have the expected taxes withheld from your retirement payments.

If you go the withholding route, you can choose to have 7 percent, 10 percent, 12 percent or 22 percent of your total benefit payment withheld. Just complete Form W-4V, Voluntary Withholding Request, and file it with the Social Security Administration.

Again, the move to a more electronic Uncle Sam means that the SSA would like you to take care of this by signing on to your Social Security online account and requesting the benefits’ withholding.

But it still will let you do so via phone. Call the SSA toll-free at (800) 772-1213 and tell the representative what percent of your monthly payment you want to withhold for taxes.

State tax due, too: In most cases, states do not tax their residents’ Social Security benefits. But nine states, for now, do tax the money.

The unlucky retirees who might have to pay their state tax collectors live in Colorado, Connecticut, Minnesota, Montana, New Mexico, Rhode Island, Utah, Vermont, and West Virginia.

The “for now” qualifier applies to beneficiaries in the Mountaineer State. This is the last year that West Virginia retirees will have to pay tax on Social Security. The taxable amount has been phasing out for the last few years and is completely eliminated in 2026.

Some of the other states, New Mexico and Colorado, for example, provide ways to reduce the Social Security tax bite.

The Land of Enchantment offers an exemption from state taxation of Social Security based on income. It applies to single New Mexico filers with less than $100,000 in income; to married couples filing jointly, surviving spouses, and heads of household with less than $150,000 in income; and to married couples filing separately with under $75,000 in income.

The Centennial State takes the same, though less generous, exemption approach. Colorado taxpayers age 55 to 64 at the end of the tax year may subtract the entire amount of Social Security benefit income included in their federal taxable income if their adjusted gross income does not exceed the following thresholds:

- $75,000 if their filing status is single; or

- $95,000 if their filing status is joint.

The cap remains at $20,000 for Colorado taxpayers whose adjusted gross income exceeds these thresholds.

Final Social Security tax note: While this post has focused on Social Security retirement payouts, there’s a final twist.

Benefits from Social Security trust funds, including survivor and disability benefits, are subject to tax rules.

However, Supplemental Security Income (SSI) payments, however, are not taxable.

Complicated, right?