Tax season means double duty for the millions who live in states that collect individual income taxes. And state taxes get even more complicated for those who live in one jurisdiction but also work at times in a locale that collects a jock tax.

The most recent and extreme example of the jock tax was Super Bowl LX played last Sunday at Levi’s Stadium in Santa Clara, California.

Officially, the levy is a nonresident tax. But it got the jock tax moniker after a tax spat 35 years ago in connection with another professional league’s championship game.

Also officially, the so-called jock tax is not limited to taxpaying athletes. If you earn income in a state that’s not your legal tax home, you likely owe tax to the state where you worked temporarily.

But jock tax is a catchier name. And it’s always more fun to look at the tax effects on generally highly-paid sports professionals. So, let’s start there.

California’s jock tax take: The Seattle Seahawks’ and New England Patriots’ players, coaches and other team members who were in Santa Clara, California, for the Feb. 8 National Football League championship game now owe 2026 taxes to the Golden State.

California, whose 13.3 percent top individuals income tax rate is the highest in the nation, assesses its nonresident tax based on the so-called duty days that such workers spend doing their jobs in the state. For the Super Bowl participants, that’s typically around 10 days.

Then there’s the NFL bonus money. The winning Seahawks athletes each earned an extra $188,000. The Patriots got $113,000 each.

Of course, not every member of either team is paid the same. So, the taxes each owes California will vary widely.

Since it’s called a jock tax, and since the teams’ biggest stars make massive salaries, it’s more entertaining (and illustrative for tax calculation purposes) to focus on the players.

Thankfully, you and I don’t have to dig out our calculators. Jared Walczak, president of Walczak Policy Consulting and a Senior Fellow at the Tax Foundation, created an online calculator that shows how different players on the Seahawks and Patriots will be taxed.

Super Bowl QB jock tax bills: Since quarterbacks tend to get the most attention, let’s look at the tax implications for the duo who faced off in Super Bowl LX.

Patriots QB Drake Maye is only in his second year in the NFL. In his case, that translates to a relatively low base salary of $915,000 and no bonus earnings.

While that’s a bummer for him personally, it’s a boon as far as his California tax bill. Walczak’s calculator says Maye owes the Golden State “just” $20,363.

It’s a different tax story for Seahawks QB Sam Darnold, who is on the other side of both the NFL championship and earnings scale. He has an annual base salary of $12.3 million, as well as an additional $4 million in bonuses for reaching performance goals this season.

Per Walzack’s calculator, Darnold’s California tax bill is $202,102. So, Darnold’s Super Bowl winning bonus of $188,000 will go to cover most of that amount.

There’s at least a bit of possible good state tax news for Darnold. If he’s a tax resident of Washington state, he won’t owe the Evergreen State any tax on his remaining NFL millions, since it taxes only the capital gains of its higher earners.

Jock tax history: The tax on nonresident earners is a decades old one that often is also levied by some city as well as state tax departments. It’s a relatively easy tax to collect, especially when it’s applied to high-profile celebrities, and adds money to state and local coffers.

As noted, visiting athletes and other nonresident entertainers — looking at you Taylor Swift and Beyoncé and all your concerts across the country — who play or perform within the taxing jurisdictions’ boundaries face the jock tax.

The jock tax moniker is obviously fitting because of its effect on high-compensated athletes. Plus, the tax practice got initial widespread recognition in 1991 when Michael Jordan’s Chicago Bulls dethroned the Los Angeles Lakers for the National Basketball Championship.

California tax officials informed Jordan that he would owe state taxes for the days he spent in L.A. In a tax tit for tat, Illinois announced that it would levy a jock tax on athletes from any state that imposed the tax on their athletes.

Now almost every state and many large municipalities have a jock tax.

Not just jocks owe: In reality, though, the jock tax applies to anyone who earns income by working in multiple states that tax individuals’ wages.

So, if you’re a middle-income consultant who spends time working in states with an individual income tax, which is most of them, you also could be a jock/nonresident tax target.

I say could, since some states have nonresident earnings thresholds that affect mostly the wealthy, notably athletes and performers. Still, for some non-famous taxpayers, the added tax from other states remains a possibility.

Another jock tax reality is that most regular taxpayers who work in various states don’t realize that it applies to them.

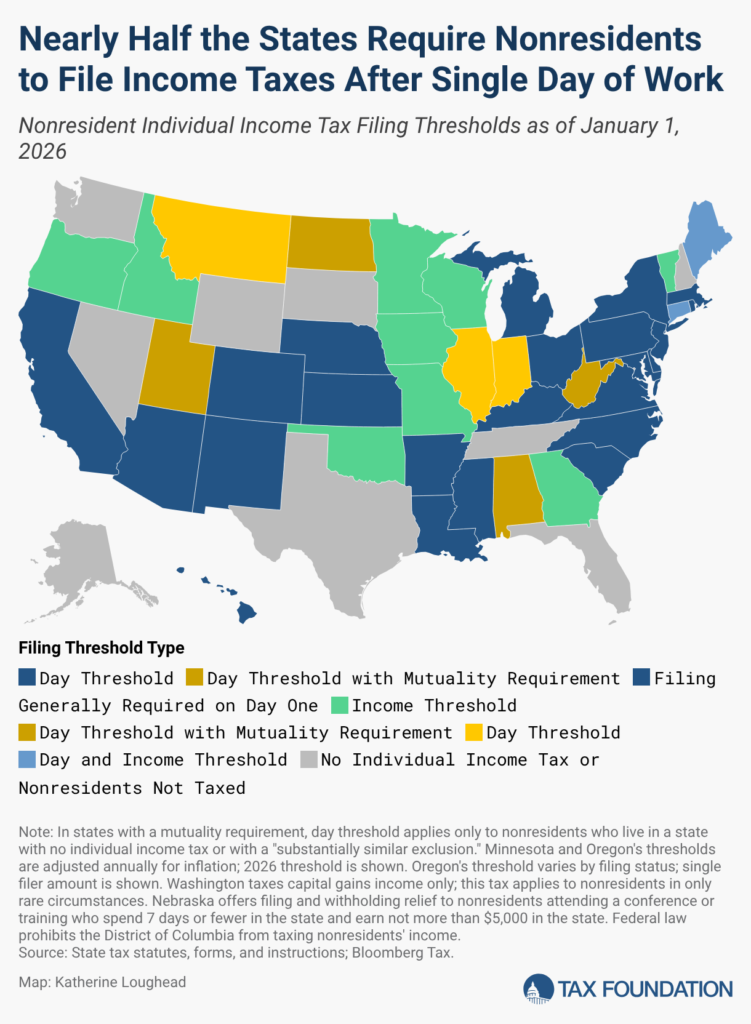

Many who technically, albeit unknowingly, are subject to the nonresident tax tend to ignore it. But if the state (or city) discovers your nonresident earnings within its border, it could come after your for payment. That could happen to taxpayers who work even one day in 22 states that no meaningful nonresident filing threshold, according to Tax Foundation research.

Congressional jock tax proposed: The wealthy athletes and entertainers who face the largest jock taxes have accountants on staff or retainer to ensure their correct compliance.

Other taxpayers, however, must deal with the tax on their own. A couple of U.S. Senators think these taxpayers need some additional help.

Senate Majority Leader Sen. John Thune (R-South Dakota) and Sen. Catherine Cortez Masto (D-Nevada) last year introduced S. 1443, which would limit states’ authority to tax certain nonresident income. Both represent states that have no individual state income tax.

The Mobile Workforce State Income Tax Simplification Act would create a 30-day work threshold for every state. The standardized month-long work requirement, the senators and the bill’s supporters in the business and tax communities, would make tax compliance easier for everyone.

“It is complicated and unfair for an individual who lives in a state like South Dakota, with no state income tax, to have to file income taxes in multiple states for simply temporarily working in those states – in some cases, for as little as 24 hours – and not be able to recover any income tax payments he or she has to make,” said Thune in introducing the bill on Aprill 10, 2025.

“Mobile workers who temporarily work outside of their home state should not find a surprise tax bill come April,” added Cortez Masto.

The bill, however, has not advanced beyond the Senate Finance Committee since its introduction.

If you’re jock tax victim, you might want to call your federal lawmakers and ask them to support the Senate proposal. It also would help to have a companion bill on the House side of Capitol Hill.

Advertisements

🌟 Search Amazon Tax Products 🌟

The text link above is an affiliate ad. If you click through and then buy a product, I receive a commission.

{kind=link}