Photo by Mike van Schoonderwalt

Some taxpayers intentionally push the filing envelope. Others simply make claims that have long caught the IRS’ eye. Here are 11 instances that could be red flags for a tax auditor.

You should take every legitimate tax break for which you qualify in order to pay the minimum about of federal tax due.

That’s not just my and tax professionals’ advice. Even the Internal Revenue Service agrees. The minimum legal payment goal is #3 in the agency’s Taxpayer Bill of Rights.

The key descriptor here is legitimate. That means you qualify for the tax deduction or credit and properly claim it. If you decide to test the tax code and IRS limits, you could be inviting unwanted attention and even a full-fledged audit.

You can avoid unwelcome IRS attention by not waving any of the following 11 audit red flags as you finish up your 2025 tax return.

Audit Perspectives Just what catches an IRS examiner’s eye depends, to borrow a favorite tax answer, on facts and circumstances. The Internal Revenue Code is complex and Congress loves to fiddle with it. That’s the case this filing season, as a variety of new One Big Beautiful Bill Act (OBBBA) tax breaks are available for eligible taxpayers. Variety also comes into play for the millions of U.S. taxpayers. Every taxpayer and tax circumstance is unique. The application of myriad tax code benefits, new and old, means we must pay as close attention to our filings as the IRS does. That said, don’t freak out if you can’t sidestep some of these audit red flags. For example, having more than just wage income, which is listed first in the potential audit list below, is common occurrence. As long as you report it accurately, and can show the IRS why it is a legal tax claim, you’re fine. But do be aware that the entry might catch the IRS’ eye. If that happens, you could at the minimum be involved in a correspondence audit. This where the IRS sends a notice asking for clarification about the questionable item. Again, just be ready to thoroughly explain why you made the claim and have material to back up the entry. |

1. You have income other than basic wages. Most taxpayers report income that shows up on Form W-2. This annual wage income statement also is copied to the IRS.

If, however, you get most or even some of your earnings each year from self-employment income or contract payments in connection with a side gig, the IRS must depend in part on your accurate report of the amount on your return.

For the 2025 tax year, payers of contract workers weren’t required to issue a Form 1099-NEC unless the earnings were $600 or more. Just like with the W-2, the IRS gets 1099 copies, too. (For your information, annual earnings threshold increases to $2,000 for the 2026 tax year.)

When the IRS doesn’t get this third-party documentation, the agency has no way, other than your honesty, to know if what you put on your return is accurate. That’s why the agency tends to give added attention to returns that include income that’s harder to document.

2. You didn’t report all your income. Forget to include some income and you’ll hear from the IRS, especially if it comes from a source that also reports to the tax man.

This includes the extra earnings mentioned in #1, as well as from something as simple as overlooking a 1099-DIV from an investment. Investment firms and brokers, like employers of full-time staff, also copy the IRS on the earnings they pay. The IRS then uses automated computer programs to match this payer information to your individual tax return. A mismatch means audit, at least in the less-invasive correspondence form.

Don’t forget about other income sources, such as prize or relatively small gambling winnings that might not trigger the need for tax documentation. All, regardless of amount, are taxable income.

How could the IRS find out if you don’t tell on your 1040? If you brag about the added taxable income on social media or your windfall was featured in your local newspaper, the IRS might discover you’re telling everyone but it about your money. Do you really want to take the chance of answering IRS audit questions just to save a few tax dollars?

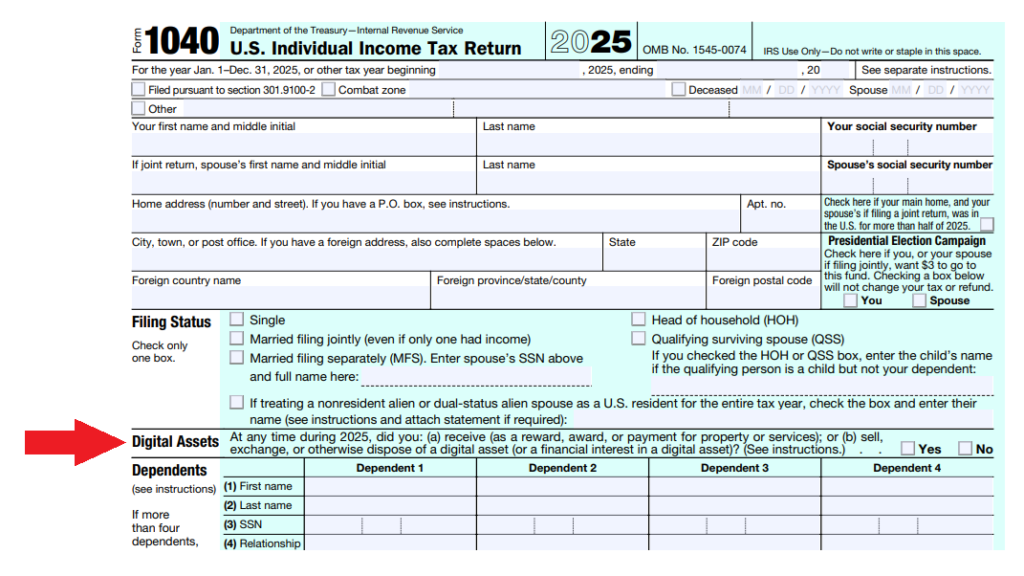

3. You didn’t tell the IRS about cryptocurrency transactions. Virtual currency continues to be intriguing for many. It’s also a potential tax audit signal.

Part of the reason is that the IRS believes unreported (and therefore untaxed) crypto transactions are a major contributor to the Tax Gap, the billions in taxes Uncle Sam is owed, but the IRS hasn’t been able to collect. To get their hands on at least some of that digital money’s tax liability, the IRS asks about crypto right near the top of Form 1040.

Specifically, Uncle Sam wants to know whether “At any time during 2025, did you: (a) receive (as a reward, award, or payment for property or services) or (b) sell, exchange, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?”

If you don’t answer this checkbox question yes or no, the IRS will ask you again, perhaps along some other inquiries about your return.

Despite cryptocurrency’s ostensible origin to make money making more egalitarian, it has complicated tax filings for many investors. So, if crypto is part of your investment portfolio, hire a tax professional who is experienced in the financial and tax components. It could save you a meeting with an IRS examiner.

4. You have a home-based business. People have always operated businesses from their homes. The IRS also has long paid close attention to such companies.

A home-office deduction is not an automatic tax audit trigger. In fact, in recognition of how many people do their jobs from home, the IRS offers a simplified way to claim this tax break. But in both cases, make sure you follow the home office deduction rules.

The main requirement is that the office space be used exclusively for work. Your office doesn’t have to be a separate room, but it must be a clearly defined area. You can’t share the space with any part of your personal life.

And note that if you’re an employee, you likely won’t qualify for the home office tax deduction. Simply doing your salaried work from home, either 40 hours a week or under a hybrid arrangement with your employer, doesn’t count even if you meet the home office requirements. Claiming this tax break as an employee, instead of an independent contractor or small business owner, is a sure way to get the IRS asking questions.

5. You reported business losses. Many home-based or other small businesses take a while to become profitable. But if your entrepreneurial operation continually runs in the red, the IRS will likely look into it.

When you start a business, the IRS expects you to do so with the goal of turning a profit. The agency generally operates on the assumption that if your so-called business doesn’t make money in three of the past five years, it’s actually a hobby. And if a business never makes money, the IRS likely will view it as a sham operation created as a way to write off a lot of expenses that really are personal, non-deductible costs.

If you are legitimately losing money, then report that. But be ready to prove that you were trying to be successful financially. Keep complete, thorough records, preferably separate from your personal finances, to prove your business intent and its unfortunate losses to the IRS.

6. You withdrew money from retirement accounts. For many, their largest savings account is their nest egg. So, when a crisis arises, either from unexpected illnesses or job loss or a major natural disaster, it’s the only place they have to turn for funds.

While the use of retirement money to pay a mortgage or rent, keep you utilities on, and refrigerator filled, using retirement funds from traditional IRA or 401(k) plans could be tax trouble.

When you take money out of these tax-deferred accounts, you owe tax on the amount. When you take the cash out before you turn 59½ you also face a 10 percent early distribution penalty.

In certain cases, distributions are allowed from workplace plans to help individuals deal with cases hardship, defined as an immediate and heavy financial need. IRS.gov also has a chart listing early retirement account withdrawals that escape the 10 percent penalty. Some of the exceptions apply only to IRAs, some apply only to workplace retirement plans, and others apply to both.

7. You claimed a whole lot of itemized deductions. Most people have always used the standard deduction amount. That number grew after 2017’s tax reform bill made some major changes to itemized deductions and greatly increased the standard deduction amounts. The OBBBA also bumped up the standard deduction amounts for the 2025 tax year.

But the Republican’s massive tax and policy measure also temporarily increased the state and local taxes (SALT) deduction amount. That prompted some filers this year to return to itemizing.

If filling out Form 1040 Schedule A gives you a larger deduction amount than your filing status’ standard deduction, then by all means itemize. Just don’t pad your allowable expenses.

The IRS in part selects returns for audit based on itemized deductions that seem excessive. A return is first screened by a computer program that scores it based on the agency’s Discriminant Information Function, or DIF. This computerized scoring algorithm compares deductions, credits, and exemptions on returns against norms for taxpayers in similar income brackets. Deviate from those amounts and an IRS auditor will give your return a personal look.

Again, the DIF factor doesn’t mean you should forgo claiming all your deductions for, say, medical costs if you had major medical expenses during the tax year. It does mean, though, that you must be prepared to show documentation of all those allowable claims.

8. You gave an unusually large amount to a charity. If you do still itemize, gifts to nonprofits are a good way to up your overall deductions total on Schedule A. But if you do make a very large donation, especially if it is a lot compared to the income you report, expect the charitable gift claim to get some added IRS attention.

True, tax law does now allow you to give up to 60 percent of your adjusted gross income (AGI) to authorized charities and claim the amount as a tax deduction. That doesn’t mean, however, that the IRS will just let the gift go by without additional examination.

So, make sure you have met the tax-deductible donation rules, which FYI change a bit for 2026 (again thanks to OBBBA). That includes having documentation of your gift from, again, a nonprofit that has met IRS muster. You don’t have to send the receipt of your donation in with your tax return. Just have it handy if the IRS asks.

9. You claimed a refundable tax credit. Tax credits are better than deductions because credits offer a dollar-for-dollar reduction of any tax you owe. And a handful of credits are refundable, meaning that if you don’t owe Uncle Sam any money, the credit could create a tax refund.

Fully refundable tax credits include the Earned Income Tax Credit (EITC). This tax credit is for working taxpayers who make lower- or moderate incomes. It’s more valuable for those with larger families, with a maximum of $8,046 available to qualifying filers of 2025 tax returns.

Partially refundable tax credits include the Child Tax Credit (CTC) and the American Opportunity Tax Credit.

The refundable portion of the CTC is claimed as the Additional Child Tax Credit (ACTC). That could provide eligible filers up to $1,700 of the $2,200 CTC as a tax refund for the 2025 tax year.

The American Opportunity Credit is worth up to $2,500 to cover qualifying higher education costs. Up to $1,000 of this education credit is refundable.

Unfortunately, for both the IRS and taxpayers, tax credit claims often are wrong, either because the tax break is complicated and confusing (looking at you EITC) or because unscrupulous filers and/or tax preparers try to cheat using refundable credits.

The IRS already must by law hold until mid-February any refunds generated on returns that include the EITC or ACTC. That extra time is for the agency to take a closer look at these claims. And while there’s no specific delay on the other credits, you can be sure IRS examiners are looking at those more closely, too.

Again, if you qualify for a full or partial refundable tax credit, by all means claim it. But be ready to show the IRS why you are rightfully seeking this tax refund-producing tax break.

10. You made easily avoidable errors on your tax return. To err is human. It also could get you audited. In fact, lots of us have technically faced an IRS exam. It’s just been in the form of the aforementioned correspondence audit. This is where the IRS catches an error on your 1040 and mails you a notice of your mistake, along with the changes the tax agency made and a bill for the additional tax you owe.

These typically are math errors, which regularly leads the annual list of the 11 most common tax errors to avoid. Note, too, note that a wrong numerical entry or transposed numbers on one line can create exponentially big tax problems if that info is transferred to another line or form.

The number error also applies to Social Security numbers. Enter wrong tax identifying digits for yourself, your spouse, or any dependents, and you could lose tax breaks based on your filing status or tax credits you claimed.

11. You relied on social media and artificial intelligence (AI) for tax advice. This red flag is not one that an IRS examiner will immediately see. It’s a warning primarily for you, dear taxpayer.

Don’t get me wrong. I am far from a Luddite. I spend way too much of my waking hours surfing the internet, and I freak out if I don’t have my smartphone within easy reach. I’m also well into my 21st year of [now-reduced] blogging about taxes.

I’ve learned over these years that while access to a wide range of information can be fun, and yes sometimes helpful, you need to be careful.

That warning gets stronger every year, as more con artists and crooks use modern technology to attain their personal, criminal goals at unsuspecting online victims’ expense.

On a less overtly insidious level, while AI is advancing, the technology is far from perfect. Remember, it’s people who are programming these mechanical givers of advice.

That’s why social media and AI advice needs to be viewed with some healthy skepticism when it comes to taxes. A lot of X/formerly Twitter and TikTok and Instagram influencers are just looking for clicks and the dollars that more eyeballs bring.

As for AI, it definitely can help refine your tax search. But as noted earlier, the tax code is complex and sometimes contradictory. Plus, as the cliché because it’s true saying pointed out, taxes are deeply personal. Unless you share with your tax chatbot all the details of your personal, financial and tax situations, the accuracy of its responses could be questionable.

And that sharing brings us back around to the issue of too much information provided to who knows who (or what). That could make you and your data prime tax scam targets. In fact, the IRS’ latest annual Dirty Dozen list warns that AI-enabled IRS impersonation by phone (robocalls, voice mimicry, spoofed caller ID) is now part of scam-related social media advice.

So be careful, not just when using online/AI guidance to complete your taxes, but in all these areas that could trigger a closer look by the IRS at your filing.

You also might find these items of interest:

- Don’t miss these 10 often-overlooked tax breaks

- Tax law changes highlight the importance of professional tax help

- Don’t panic. That’s the first move to make when you get an IRS tax notice

Advertisements

🌟 Search Amazon Tax Products 🌟

The text link above is an affiliate ad. If you click through and then buy a product, I receive a commission.

{kind=link}