Children are expensive. So are higher education costs. And these expenses often coincide, as in the cases of new moms with higher education degrees who will celebrate their first Mother’s Day this Sunday. Tax breaks can help both parents, students, and parents who are/were students.

…

Some people question the wisdom of having children in this day and age. But the U.S. Census Bureau says that nowadays, formally educated women are choosing motherhood.

Notably, more women with a bachelor’s or higher degree are having their first child.

The percentage of first-time mothers who graduated college has jumped from 75 percent in the early 1990s to roughly 85 percent this decade, according to a recent Census report.

These women are among the moms we’ll honor on Mother’s Day. It’s this coming Sunday, May 10, in case you still need to get your mom a gift!

A variety of tax help: In addition to going to college, Census research shows that this growing sector of new moms also tends to be married.

Analysts say maternal educational differences highlight a growing divide in family stability. Women who are on more solid financial footing tend to be in stable personal pairings, such as marriage, than women who are have less socioeconomic support.

Of course, while data gives us an overview of family groups, it is just numbers. Real people often contradict or defy official figures.

Women who aren’t in formal, state-sanctioned relationships or who are happily single have children all the time. They also find ways, regardless of their financial situations, to make sure their families are okay.

But it’s also true that sometimes we all need some help. In many cases, our federal relative Uncle Sam offers assistance, often through tax breaks.

Here’s a look at some of the more popular ways the Internal Revenue Code can help ease the costs of going to school and/or raising a child.

Tax breaks for filers with children: Children are expensive. Parents and those of us without kids agree on this financial fact.

We, as well as the federal government, also agree that the welfare of our country’s youngest citizens is crucial to us all. That’s part of the tax code includes ways to help cover child-related costs.

The most popular is the Child Tax Credit (CTC). The CTC is worth up to $2,200 per qualifying child. Filers with little or no federal income tax liability may qualify for the Additional Child Tax Credit, which is worth up to $1,700 per qualifying child depending on your income.

As a credit, these tax breaks offset dollar-for-dollar any tax you owe.

The CTC is a nonrefundable tax credit, meaning if the amount you qualify for is more than you owe, it will zero out your tax liability but you lose any credit in excess of your bill. The ACTC, however, is refundable. Any extra ACTC will come back to you as a refund.

Working parents who pay for child care also may be able to get some tax help from the Child and Dependent Care Credit. This nonrefundable tax credit is worth up to can provide a credit for a portion of child-care expenses of up to $3,000 for one child or up to $6,000 for two children.

The actual Child and Dependent Care Credit is a percentage of those amounts, based on your income, starting at 20 percent and going to 50 percent for the 2026 tax year (up from the prior 35 percent).

Families that add members through adoption also can get some tax help.

The Adoption Tax Credit is worth up to $17,280 for each adoptee in 2025, but the One Big Beautiful Bill Act added a provision making up to $5,000 in qualifying adoption expenses refundable. For the 2026 tax year, the adoption credit increased to $17,670.

Educational tax benefit lessons: The tax code also offers a variety of help for parents going to school, as well as for their children.

School-related tax breaks include credits, deductions, income exclusions for workplace provided benefits, and tax-advantaged savings plans. My earlier post “A lesson plan for maximizing 8 education tax breaks” has more on some of the more popular one, but three are worth mention here, too.

The American Opportunity Tax Credit (AOTC) can be worth a maximum benefit of up to $2,500 per eligible student. It’s available for costs related to pursuing a degree or other recognized education credential.

The AOTC also is a partially refundable credit. So, if under certain circumstances the AOTC reduces students’ tax liability to zero, they could receive up to $1,000 of excess credit as a refund.

The Lifetime Learning Credit (LLC) can be claimed by college students, but it also is available to a wider range of students. However, this educational tax credit is nonrefundable.

Still, the LLC is worth checking into since, as its name implies, it can be used to cover costs of studies beyond the first four years at a university. That includes graduate students looking to help pay additional studies’ tuition and fees, as well as by individuals who are not in school, but are taking courses to acquire or improve job skills.

The exact LLC tax credit amount is calculated as a percentage of qualifying education costs. That’s 20 percent of the first $10,000 in tuition expenses paid per year, up to a maximum credit of $2,000.

Parents looking to save for their youngsters’ higher education should consider a 529 plan. These accounts, created by Congress in 1996, officially are designated as a “qualified tuition program” in the Internal Revenue Code (IRC). But they are popularly known by their numerical name, which comes from the tax code section 529 that covers their associated tax benefits.

There are two types of 529 plans, a tuition prepayment plan, and a savings (really an investment) plan to which you contribute money to be used later to pay for a student’s qualified higher education costs. The tax-favored savings plan option is the more popular choice, and is the one that typically is referred to in 529 plan discussions.

Contributions to a 529 education savings plan grow tax-deferred, allowing the money to compound more quickly since you don’t lose a portion of it to taxes. That tax benefit extends to qualified withdrawals.

As long as you use 529 plan funds to pay for qualified education expenses, Uncle Sam won’t collect a dime. Also, in some instances 529 funds can be used to pay for non-college educational costs.

All of these child and education related tax breaks have specific requirements, so take care in claiming them. In fact, it’s usually worth speaking with a tax professional to ensure that you get the most of all tax breaks for which you, as a parent or student (or parent of a student) qualify.

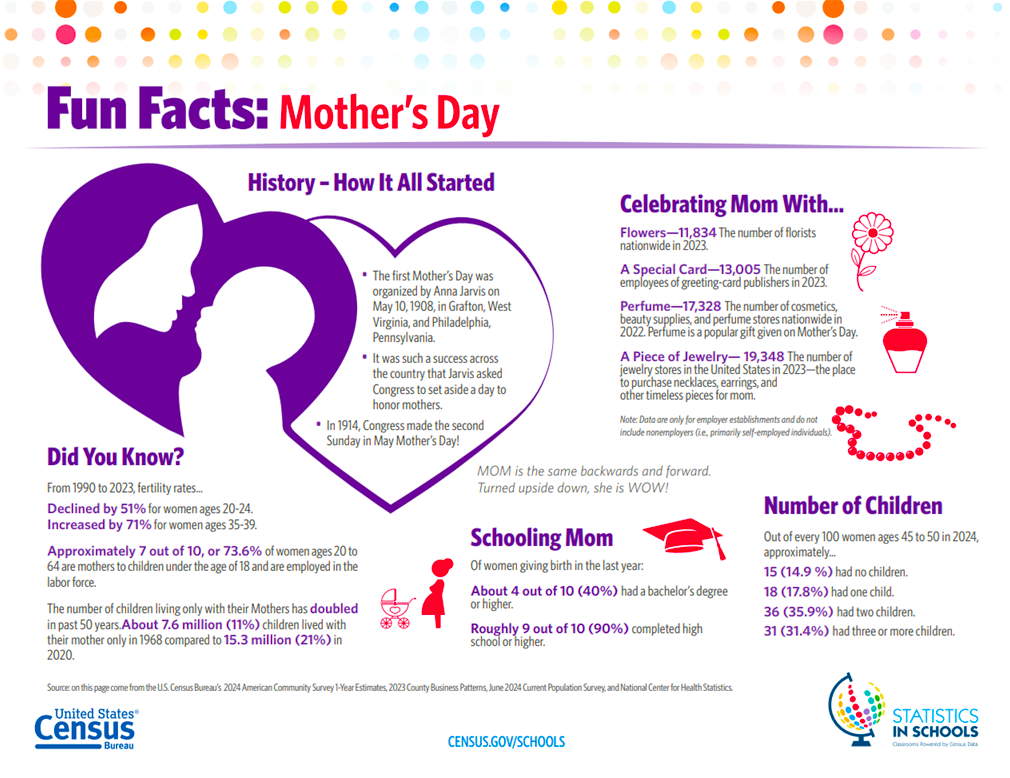

Mother’s Day fun facts: The first Mother’s Day was organized on May 10, 1908 in West Virginia and Philadelphia. It became an official nationwide holiday on the second Sunday in May in 1914.

The Census Bureau graphic below has some more interesting Mother’s Day fun facts.

…

…

Mother’s Day gift figures and suggestions: Before wrapping up this post, I must return to the earlier reminder of fast-approaching Mother’s Day. Have you gotten your mom a Mother’s Day gift, or planned for a special celebration this coming Sunday?

You won’t be alone in celebrating all your mom has done for you, whether you’ve planned the special day for a while or are a last-minute gift shopper.

Consumer spending on Mother’s Day is expected to reach a record $38 billion this year, according to the annual survey released by the National Retail Federation (NFR) and Prosper Insights & Analytics.

The projected 2026 spending amount handily beats last year’s total of $34.1 billion and exceeds the previous Mother’s Day spending record of $35.7 billion set in 2023.

“Mother’s Day remains a priority for many Americans, and they plan to lean into the holiday despite current economic uncertainty. Consumers are gifting from the heart, seeking unique gifts that create lasting memories for the mothers in their lives,” said NRF Chief Economist and Executive Director of Research Mark Mathews.

The per-person spending also is projected to be one for the record books. The NRF/Prosper findings show consumers plan to spend a record average of $284.25 on gifts, up from $259.04 last year and besting the previous record of $274.02 in 2023.

Jewelry leads Mother’s Day spending at $7.5 billion, followed by special outings at $6.4 billion and electronics at $4.4 billion.

One thing hasn’t changed, though. Flowers remain the most popular gift category, with 75 percent of shoppers planning to purchase a bouquet for mom. Total floral spending this Mother’s Day is projected to reach $3.2 billion.

But don’t fixate on prices. Your mom doesn’t expect you to go overboard this Sunday.

In fact, every year more than half of moms surveyed say that just spending time with their children is the best Mother’s Day gift of all.

…

Advertisements

🌟 Search Amazon Tax Products 🌟

The text link above is an affiliate ad. If you click through and then buy a product, I receive a commission.

{kind=link}