It’s never too early for children to learn solid money lessons. The new Trump Account option, which became available on July 4, now offers them a tax-advantaged way to invest. (Curated Lifestyle for Unsplash+)

…

Trump Accounts finally are here.

The new tax-favored savings vehicle for youngsters was created last July 4 as part of the One Big Beautiful Bill Act (OBBBA). It’s actual operation was delayed a year so that the federal government could establish the mechanism for families to take advantage of the accounts.

That technically happened on Saturday, July 4.

But today, the first business day after the accounts’ launch, is when most families who haven’t already started the enrollment process will get their introduction to the accounts.

Here’s a look at the plans and the steps to take if you want to create a Trump Account for your child.

Account overview: A Trump Account is a tax-advantaged retirement savings option for U.S. citizens age 17 and younger.

The account essentially is a starter IRA. However, it doesn’t strictly follow the regular traditional or Roth IRA rules. Trump Accounts have different contribution limits, investment rules, distribution guidelines, and other requirements.

For example, contributions to Trump Accounts are made with after-tax dollars. This makes them similar to a Roth IRA, where you don’t get a tax deduction for the contributions.

However, the accounts’ earnings are tax-deferred, as with traditional IRAs. So, withdrawals ultimately are taxed as ordinary income.

And speaking of IRAs and Trump Accounts, note that they are not mutually exclusive. A young person who has a weekend or summer job can still open an IRA and contribute to that retirement account, as well as put money into the new Trump administration plan.

Account eligibility: A Trump Account can be established for a youth who is younger than 18 at the end of the calendar/tax year. The youngster also must be a U.S. citizen. That allows the Social Security Administration to issue the child a Social Security number.

Creating an account: You set up a Trump Account by filing Form 4547, Trump Account Election(s), with the Internal Revenue Service.

The account is established in the minor child’s name and with the youth’s Social Security number. The parent or legal guardian who submits the Form 4547 acts as the sole custodian of the Trump Account until the youngster turns 18 (more on this later).

The Treasury Department and IRS recommend you complete and file Form 4547 electronically. You have two options here.

If you have an IRS individual taxpayer online account, you can fill out and submit Form 4547 there. It’s probably worth doing this, since you’ll need an ID.me account — this is identity verification platform the IRS and other federal government agencies use — to open your online taxpayer account and you’ll need that ID.me info later to activate the Trump Account.

Or you can use the Trump Account app to open an account for an eligible child. Even if you don’t use the mobile app to open a Trump Account, you might want to download it. The app will help you track and manage account activity.

After filing Form 4547, the Treasury Department or its agent will send you instructions to authenticate your identity and officially activate the account.

Once you set up the Trump Account, the Treasury Department and its authorized financial service providers may contact you by email, text message, or automated phone call regarding the account’s activation and administration.

Initial activation emails will come only from no-reply@TrumpAccounts.Treasury.gov. Official emails will come from addresses ending with @trumpaccount.com.

Confirming that any Trump Account outreach is from legitimate government contacts is just the first security step. Beware of additional account requests, which could be crooks looking to take advantage of the new accounts to steal your money and financial identity.

Treasury and its authorized service providers will never ask you to disclose passwords, one-time verification codes, or other sensitive account credentials by email, text message, or phone call. If you’re ever asked to do that, don’t. It’s a scam.

Bonus birth date contribution: The OBBBA created a temporary one-time contribution pilot program to boost participation in Trump Accounts.

The federal government will add $1,000 to Trump Accounts that are opened for qualifying infants who are born after Dec. 31, 2024, and before Jan. 1, 2029.

The Social Security Administration is working on a process to enroll newborns in the account.

The plan will allow parents who use the SSA’s Enumeration at Birth program to register their children for Social Security numbers while the babies are still in the hospital to also sign up for a Trump Account. Parents who use this hospital option won’t have to fill out Form 4547 later or check a box on their tax returns to open an account.

Contribution limits: OK, you’ve decided to open a Trump Account for your child. And Uncle Sam’s one grand contribution is a nice start. But now there’s the follow-up financial question. How much can you put into it?

You can deposit a maximum of $5,000 a year into the account. That contribution cap will be adjusted for inflation beginning in 2028.

Contributions may be made by parents, relatives, friends, and employers.

Employer and employee salary reduction contributions also are allowed. These are subject to a $2,500 limit per employee. These contributions are not included in the employee’s gross income, provided they are made through a formal workplace program.

An employer’s contributions, however, do count toward the $5,000 maximum annual contribution limit.

Some state government and philanthropic organizations/charitable individuals also may contribute to the accounts. These contributors are not subject to the $5,000 annual limit.

Note, however, that the nonprofit contributions generally are limited to certain parts of the country or based on specific income levels. For example, Michael and Susan Dell — yes, of the Dell computer fortune — have pledged $6.25 billion to support Trump Accounts.

The Dells will add $250 to each the accounts opened for roughly 25 million children younger than age 10 who aren’t eligible for the federal $1,000 contribution. To qualify for the funds, the children must live in Zip codes where the median household income is below $150,000.

The Trump Account website has a list of companies and charities that are, so far, contributing to the accounts.

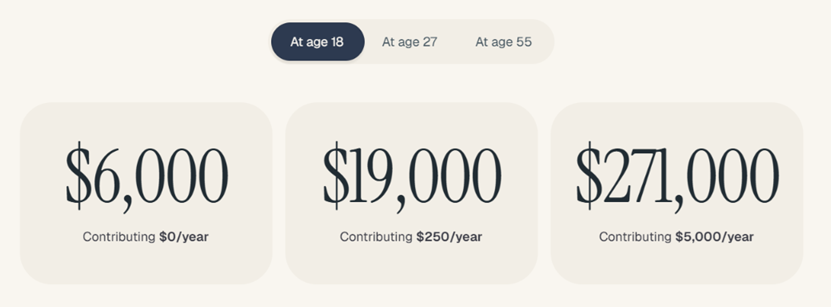

The White House touts the potential financial windfall the accounts can provide simply via contributions. It displays the projected amounts at various stages in a Trump Account owner’s life, shown below, on TrumpAccounts.com.

Account investment choices: Trump Account earnings could be more if the investments into which they are placed do well. So, just what are an account owner’s choices?

The new tax law says funds must be invested in mutual funds or exchange-traded funds (ETFs) that track the return of either the S&P 500 Index or another index that consists of equity investments primarily in U.S. companies.

Management fees are capped at 10 basis points (0.10%).

The current default account where all Trump Account contributions will go is the ETF State Street SPDR Portfolio S&P 500 ETF (SPYM). Treasury said SPYM was selected “to provide broad exposure to the U.S. stock market while maintaining expenses well below the statutory fee limitation.”

Treasury has also selected the following additional low-cost index ETFs for the Trump Accounts investment lineup:

- iShares Core S&P 500 ETF (IVV)

- Vanguard Total Stock Market ETF (VTI)

- State Street SPDR Portfolio S&P 1500 Composite Stock Market ETF (SPTM)

- iShares Core S&P total U.S. Stock Market ETF (ITOT)

However, these additional funds are not yet available for Trump Account contributions.

“In the coming months, Treasury expects to make available functionality that will allow parents or guardians to choose how to allocate funds across the additional investment options. Until that functionality is available, all contributions will remain invested in the default [SPYM] fund,” according to Treasury officials.

Access to account money: A nice account balance will be a welcome benefit. But when will it be available? Not for a while, at least if you want to maximize the tax benefits.

Money cannot be withdrawn until the young person for whom the Trump Account was opened turns 18, the legal adult age in most states. Upon celebrating that birthday, the young account owner gets full access and control over the account’s balance.

But unless the money is used for certain purposes, distributions before the account owner is age 59½ are subject to a 10 percent early withdrawal penalty. This is the same penalty assessed on traditional IRA pre-retirement distributions.

Trump Account owners can avoid the early-withdrawal penalty by using assets to pay for certain authorized expenditures. These include eligible education expenses, the purchase of a first home, certain medical costs, and other exceptions allowed under traditional IRA rules.

Also at age 18, account holders will be able to transfer their Trump Account to a traditional IRA. Once in that account, they can convert it to a Roth IRA.

For a young account owner, switching it to a Roth could be a wise move, since that account provides tax-free retirement distributions that are not subject to required minimum distribution (RMD) rules.

Financial advice recommended: Of course, any tax or money move requires you take all your personal financial components into account.

For the traditional IRA to Roth conversion possibility, remember that you’ll have to pay tax on the converted funds. If you use the IRA funds to pay taxes, that will reduce your overall retirement savings.

So again, it’s something to consider, and to do so after getting advice from a reputable tax professional and/or financial adviser.

That financial expert also can offer guidance on how Trump Account money might affect a student’s quest for other educational assistance.

Currently, a young person’s assets, which the Trump Account will be when they turn 18, come into play when they use the Free Application for Federal Student Aid (FAFSA) to find financial help to pay for college. The U.S. Department of Education has not confirmed how Trump Accounts will be treated in the FAFSA.

The wider variety of a 529 plan, which also has tax advantages (sometimes at the state level, too) might be a better, or complementary, choice when looking ahead on how to pay for college. In some cases, families find a tax-deferred Coverdell education savings account meets their needs.

That’s not to say don’t open a Trump Account. That’s especially true if your child is eligible for the one-time $1,000 bonus from Uncle Sam.

The accounts also offer some retirement flexibility, and their ETF focus is a bonus for individuals who are not comfortable with stock market investing.

Look at a Trump Account as a part (or a start) of an overall tax and financial strategy. And if you’re not sure how or whether it fits into your and your child’s needs, get some help before making a decision.

You also might find these items of interest:

- Problems with Trump Savings for children

- A lesson plan for maximizing 8 education tax breaks

- 7 financial gifts for new graduates, some with tax benefits

…

Advertisements

🌟 Search Amazon Tax Products 🌟

The text link above is an affiliate ad. If you click through and then buy a product, I receive a commission.